Business Rates & Valuation Guide (NDR) – ScotGov

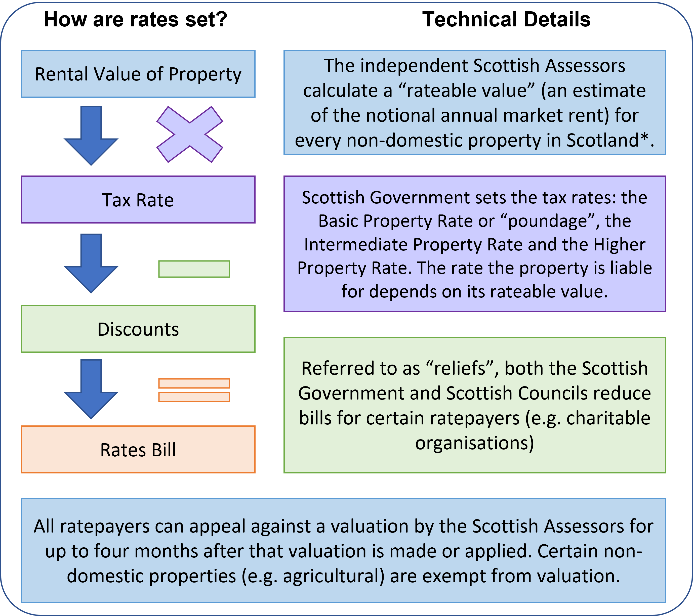

Non-Domestic Rates (NDR), often referred to a business rates, are levied on non-domestic “lands and heritages” – properties that are not dwellings, in the private, public and third sectors. NDR are levied on the occupier of non-domestic properties (or owner in the absence of an occupier, and councils have the power to charge the owner in prescribed cases of rates avoidance). Councils collect and administer NDR including reliefs.

NDR bills are calculated by multiplying the rateable value of a property by the tax rate and adjusted for any eligible reliefs. The tax rate is known as the “poundage” (i.e. a pence per pound charge, for instance a 50p poundage means that the tax rate is 50% of the total rateable value of a property).

To note, the first stage of the appeal process is to make a proposal to the assessor. Further detail about deadlines to make proposals and appeals are available here: Non-domestic rates appeals - mygov.scot

Non-domestic properties (unless they are exempt from rating such as agricultural lands and buildings) are given a rateable value and entered onto the valuation roll by independent Scottish Assessors, at which point they become liable for NDR.

Properties’ rateable values are based on the notional market rental value that a property could be expected to attract on the open market and are reassessed every three years at ‘revaluation’. The next revaluation is on 1 April 2026.

To ensure that all properties are valued on the same basis, rateable values are benchmarked against the same date – the ‘tone date’. The tone date (or ‘valuation date’) for the 2026 Revaluation is 1 April 2025. The Assessor may, generally on or around the tone date, ask for information about rental or other valuation information on a property to help inform valuations by issuing Assessor Information Notices (AINs).

To avoid a civil penalty, responses to AINs must, by law, be returned to Assessors within 28 days of their request.

Further detail on civil penalties can be found here: Fines for not giving information - mygov.scot

Self-catering accommodation properties in particular are subject to an annual audit. Audits to cover financial year 2024-25 will be carried out during the year. It is important to return information to Assessors on time otherwise those properties will be deleted from the Valuation Roll and entered in the Council Tax Valuation List, and liable for Council Tax from 1 April 2024.

If the required evidence is not provided to the Assessor within 56 days of a request being made, or 56 days after the end of the financial year (whichever is later), the self-catering accommodation will be deleted from the Valuation Roll and entered in the Council Tax Valuation List and liable for Council Tax.

Businesses can now access a short guide to Non-Domestic Rates and Reliefs for 2025-26, including links to further information and a timeline for the 2026 revaluation.